Banks ramp up foreclosure activity in Las Vegas

After sharply pulling back last year, banks are ramping up foreclosure activity in Las Vegas again.

Lenders issued an average of about 500 default notices per month in the fourth quarter last year, up from just 32 a month in the third quarter and 380 per month in the first half of 2017, according to figures from housing tracker Attom Data Solutions.

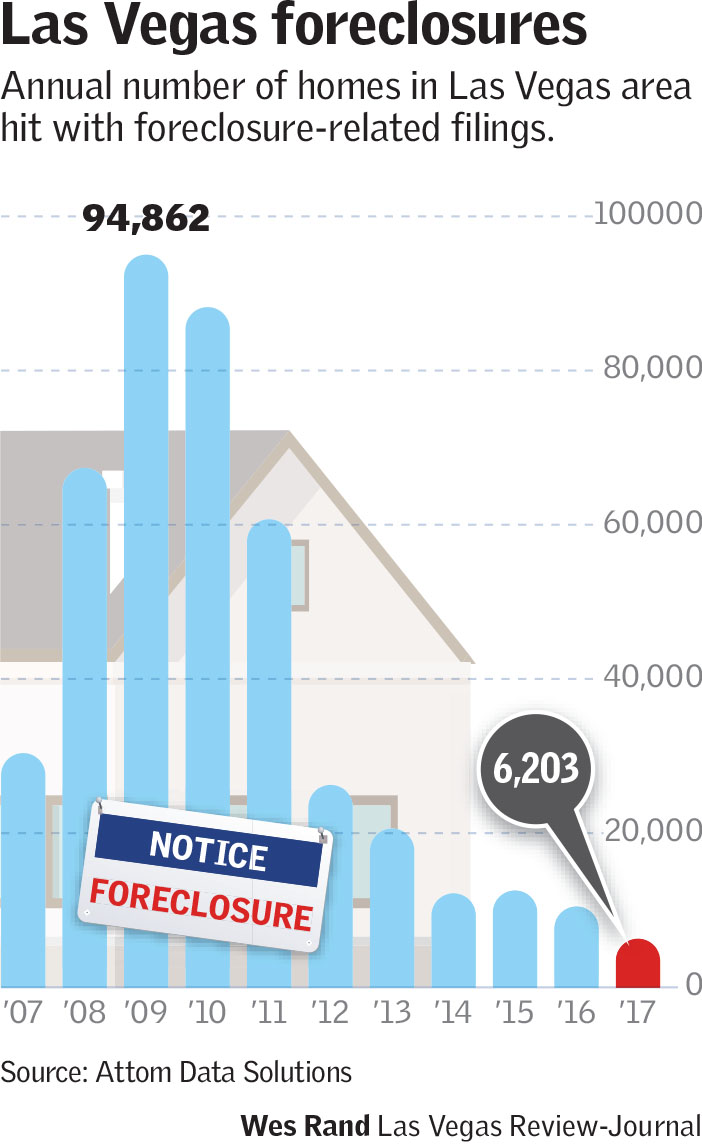

Overall in Las Vegas, the number of homes hit with foreclosure-related filings plunged 40 percent last year.

But before you start cheering that Las Vegas’ housing market has FINALLY recovered from the brutal recession that all but toppled the local economy last decade, we should note, as we have before in this column, that last year’s drop came after a new foreclosure law kicked in.

The law, Senate Bill 490, took effect June 12 — the same day Gov. Brian Sandoval signed it — and made permanent the state’s Foreclosure Mediation Program. It also shifted the program’s oversight to Home Means Nevada, a state-launched nonprofit that had effectively shut down early last year.

Lenders slammed the brakes on repo activity while waiting for the program’s new administration to take shape, industry pros have said.

Home Means Nevada is now fully operational and started issuing certificates Nov. 1 that let lenders proceed with foreclosures, board president Shannon Chambers said.

Foreclosures were sliding in Las Vegas before the law took effect. But the drop last year “wouldn’t have been quite as dramatic without the legislation,” said Daren Blomquist, Attom’s senior vice president of communications.

Now, banks are “starting to play catch-up,” he said.

Well, at least with default notices, he pointed out.

Locally, foreclosure auctions were scheduled an average of about 69 times a month in the fourth quarter. That’s compared to 71 a month in the third quarter and 235 a month in the first half of the year, Attom’s numbers show.

Meanwhile, lenders repossessed an average of about 160 homes a month in the fourth quarter, up from 100 in the third but still well below the monthly average of 293 in the first half of 2017.

Las Vegas was the foreclosure capital of America after the real estate bubble burst, and empty homes with blue-taped repo notices became an all-too-common sight in the valley.

From 2008 through 2010, lenders issued an average of 5,300-plus default notices monthly against local homes and repossessed an average of more than 2,600 a month, according to Attom’s figures.

Bargain-hunting flippers and other investors packed Las Vegas’ foreclosure auctions after the market crashed. But as repos dropped, the discounts and auction crowds shrank with it.

One investor who did not want his name published said he rarely goes to auctions anymore because “there’s no inventory.”

He plans to stop flipping houses in the valley after he unloads his current properties and is looking to do business out of state. Also, homes that do come up for auction in Las Vegas get bid up to “retail value,” he noted.

“The discount’s not even there anymore,” he said.

Contact Eli Segall at esegall@reviewjournal.com or 702-383-0342. Follow @eli_segall on Twitter.