Las Vegas’ home price growth flying past US average

Capping a heated year for housing, Las Vegas prices ended 2021 rising at a faster clip than the U.S. overall.

Southern Nevada house prices in December were up 25.5 percent from a year earlier, compared with a gain of 18.8 percent nationally, according to the S&P CoreLogic Case-Shiller index released Tuesday by S&P Dow Jones Indices.

This marked the seventh consecutive month that prices in Las Vegas accelerated faster than in the country at large.

Phoenix home values rose fastest among the 20 markets tracked for the report, skyrocketing 32.5 percent year over year.

Overall, prices are at all-time highs across all 20 markets, Craig Lazzara, managing director at S&P Dow Jones, said in a news release.

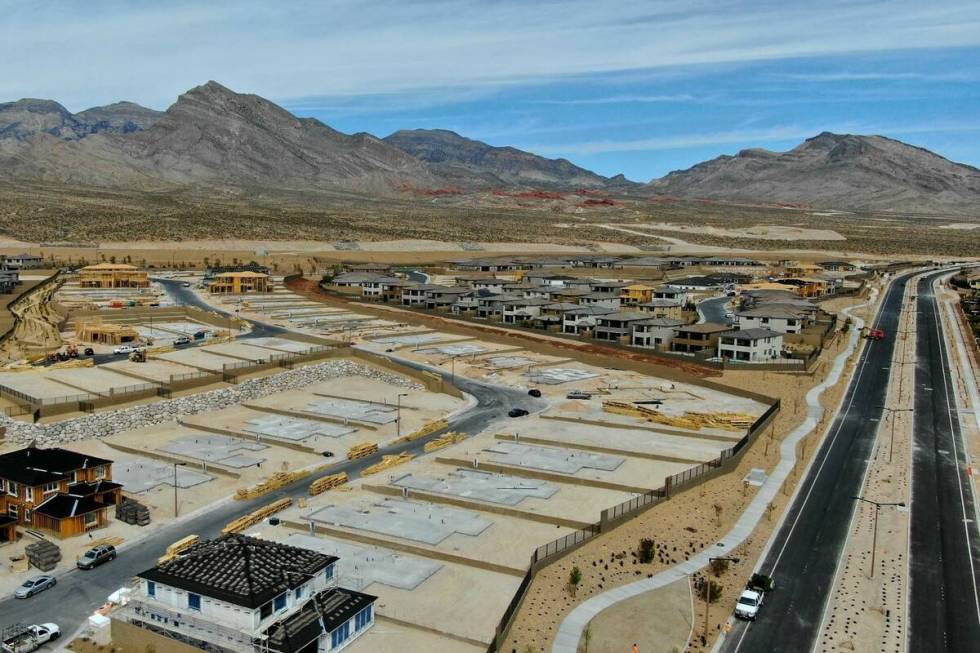

Despite high unemployment sparked by the coronavirus outbreak, Las Vegas’ housing market accelerated last year with rapid sales and record-high prices, fueled largely by rock-bottom mortgage rates that have let buyers stretch their budgets.

The frenzy looked largely the same as in other U.S. cities, marked by tight inventory, multiple offers and sellers firmly in control as people tried to buy a place amid low borrowing costs.

‘Scarce selection’

Across the U.S., limited inventory and “persistent demand” kept competition elevated at year’s end, Matthew Speakman, an economist with listing site Zillow, said in a statement Tuesday.

The “scarce selection” of available homes for sale has “likely dissuaded some would-be shoppers from testing the market,” but overall, buyer demand “remained very strong by historic norms,” he said.

Among the markets tracked for the Case-Shiller report, 15 showed higher year-over-year price jumps in December than in November.

Selma Hepp, deputy chief economist at housing tracker CoreLogic, pointed to this “re-acceleration” and said house hunters “may have been rushing” in anticipation of higher mortgage rates.

The average rate on a 30-year home loan in December was 3.1 percent, up from 2.68 percent a year earlier, according to mortgage finance giant Freddie Mac.

Nonetheless, as rates keep going up, “budget-constrained buyers will face more challenges, likely leading to some waning demand,” Hepp said.

The average rate on a 30-year mortgage last month was 3.45 percent.

‘Very strong seller’s market’

Job losses sparked by the pandemic were heavily concentrated in service sectors. White-collar — and likely higher-earning — workers often kept their jobs but started working from home, and with mortgage rates at historic lows, many people tapped cheap money to buy a place, helping fuel America’s unexpected housing boom.

Southern Nevada, long a popular place for people to move to, has seen more out-of-state buyers than usual during the pandemic, especially from pricier markets such as California, as people sought more space amid widespread work-from-home arrangements.

On the resale side last year, buyers showered Las Vegas Valley homes with offers and routinely paid over the asking price, and median sales prices set new all-time highs practically every month.

Homebuilders in the valley put buyers on waiting lists, regularly raised prices and in some cases drew names to determine who could purchase a place.

All told, the buying binge created an extreme seller’s market, making it increasingly difficult to purchase a home and sparking affordability concerns.

The hot streak is far from over, as Southern Nevada started 2022 with prices at another all-time high.

The median sales price of previously owned single-family homes — the bulk of the market — was a record $435,000 in January, up 26.1 percent, or $90,000, from January of 2021, trade association Las Vegas Realtors reported.

Randy Hatada, owner of Xpand Realty & Property Management, said earlier this month that he’s not seeing the same volume of offers that he did in the past year or so, but sellers are still fielding offers above their asking price.

Las Vegas’ low supply of available listings forces people to play a bidding game or to come in “very aggressively” to land a house, he said, noting properties are “still going quickly.”

Just 1,821 single-family homes were on the market without offers at the end of January, down 19.1 percent from the month before and 21.3 percent year-over-year, according to LVR.

“It’s still a very strong seller’s market,” Hatada said.

Contact Eli Segall at esegall@reviewjournal.com or 702-383-0342. Follow @eli_segall on Twitter.