6 biggest casino deals on the Strip in 2022

A number of casino operators changed up their real estate portfolio this year with sales, acquisitions and leasebacks — showcasing a flurry of activity after the short but steep economic fallout caused by the COVID-19 pandemic.

And a number of those deals, announced last year, have closed in 2022.

Here are six of this year’s major deals on the Strip, including one anomaly.

Las Vegas Sands shifts focus

Las Vegas Sands Corp. officially exited the Las Vegas market in February, after Apollo Global Management Inc. took over the reins of its three Strip assets — The Venetian, Palazzo and The Venetian Expo.

Las Vegas Sands is still headquartered in Las Vegas but it has turned its focus on investments in Macao, where it is a market leader, and Singapore. It is also concentrating on other investments in the U.S. with prospects in Texas, Florida and New York.

Apollo, Sands and Vici Properties Inc. first announced the $6.4 billion deal in March 2021.

Under terms of the deal, Apollo paid a total of $2.25 billion. New York-based Vici, a real estate investment trust affiliated with Caesars Entertainment Inc., paid $4 billion in the transaction. It now owns all of the real estate assets while Apollo operates the properties.

Apollo is no stranger to the gaming industry. It acquired Caesars Entertainment, then called Harrah’s, in 2008 with private equity firm TPG Capital then invested $2.4 billion into Caesars’ Las Vegas operations. The firms sold their remaining stake in Caesars in 2019, two years after Caesars’ main operating unit emerged from bankruptcy in 2017.

The new Venetian owners have since found the resort has substantially outperformed expectations since the acquisition, which it shared during a recent Nevada Gaming Commission meeting. The company doled out $1,500 bonuses to its 7,000 employees in early December, and told the commission that it plans to invest $1 billion in the property in the next three to four years.

Palms makes history

When the Palms reopened on April 27, it came back to much fanfare and it carved out a chapter in Las Vegas’ history book. After the off-Strip casino-resort was dark for more than two years, it opened as the first resort in Las Vegas to be owned and operated by a Native American tribe.

The San Manuel Band of Mission Indians, the tribe that operates the Yaamava’ Resort and Casino in Highland, California, purchased the 21-year-old property from Red Rock Resorts for $650 million in May 2021.

It revamped the property with a new cafe, furnishings and upgraded the back-of-house features.

Not much else was needed, as the property underwent a $690 million facelift in 2019, while under Red Rock Resorts’ ownership. Red Rock invested heavily in the property’s daylife and nightlife components, including the Kaos Nightclub.

Palms General Manager Cynthia Kiser Murphey told the Review-Journal in September that now the focus is on attracting Las Vegas locals as well as its Southern California clientele.

Cosmopolitan changes hands

The Cosmopolitan of Las Vegas officially became an MGM Resorts International property in May, a deal that extended MGM’s footprint on the Strip.

Blackstone sold The Cosmopolitan for $5.65 billion in September 2021 with MGM purchasing the resort’s operations for $1.63 billion and entering into a 30-year lease agreement. The Cosmopolitan’s real estate was sold to a group of new investors, though Blackstone retained an ownership stake in the property.

Blackstone purchased The Cosmopolitan in 2014 for $1.73 billion then invested $500 million into renovating its roughly 3,000 guest rooms and luxury suites as well as upgrading the bar and restaurant offerings.

Bally’s takes over Tropicana

In another sale-leaseback agreement, Bally’s Corp. closed on its $308 million purchase of the Tropicana Las Vegas from Penn Entertainment Inc. in September. The deal was first announced in April 2021.

Bally’s is expected to pay the property’s land owner Gaming and Leisure Properties Inc., a REIT affiliated with Penn Entertainment, $10.5 million annually in a 50-year lease agreement.

The Tropicana could also see another big change in its future. The 35-acre site, on the south end of the Strip, is being considered as the site for an MLB stadium project for the Oakland Athletics. Bally’s CEO Lee Fenton said last month that the Tropicana is still “very much in the cards,” as a potential site.

The Mirage gets a new owner

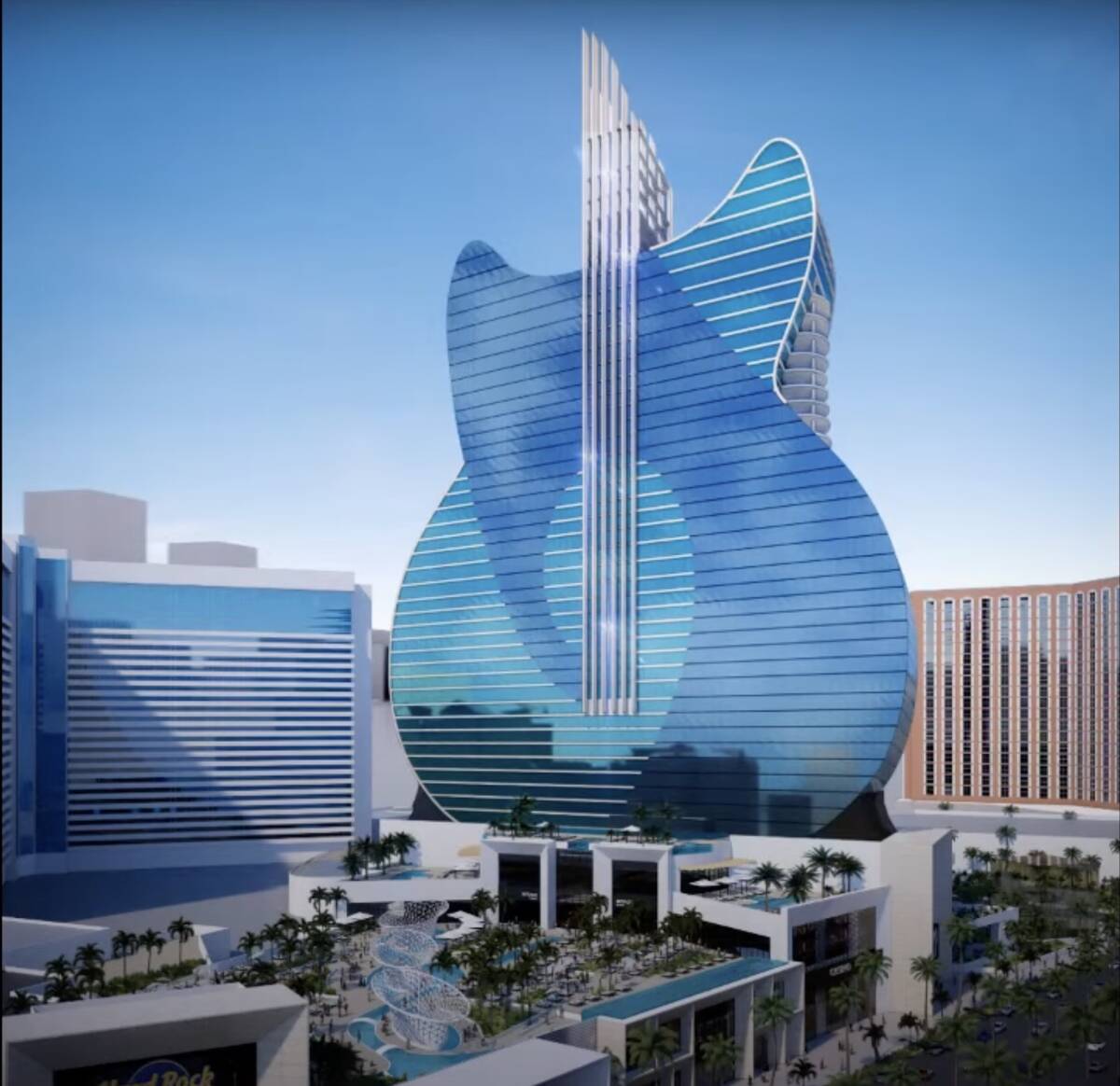

On Monday, Hard Rock International officially closed its $1.08 billion purchase of The Mirage from MGM Resorts International. The Nevada Gaming Commission approved its licensing to operate the hotel-casino last week.

Hard Rock, owned by the Seminole Tribe of Florida, said it plans to gut the three-wing property and spend billions to expand and upgrade it with the Hard Rock branding, starting in late 2023 or 2024.

When the resort expands, it will go from 3,044 rooms as The Mirage to 3,640 rooms as the Hard Rock; 836 slot machines to 2,000; and 51 table games to 212. The casino will be enlarged from 94,000 square feet to 174,000 square feet while the convention space will grow from 200,000 square feet to 283,000 square feet. The theater will go from 3,278 theater seats to 6,265 and 18 food and beverage outlets to 21.

The new owners also plan to replace one iconic feature — The Mirage volcano — with an all-suites tower in the shape of a guitar.

Caesars changes its mind

Caesars’ decision to not make a deal is what landed the company on the list.

For more than a year, Caesars executives publicly floated the idea of selling one of its Strip resorts, though it had talked about selling a Strip asset dating back to when Eldorado Resorts announced it was acquiring and merging with Caesars in 2019. When the COVID-19 pandemic hit a year later, executives said at the time it would delay those plans while the hard-hit gaming and tourism industries bounce back.

Meanwhile, Wall Street analysts identified the Flamingo and Planet Hollywood Resort as two prime candidates for a sale.

Caesars CEO Tom Reeg told investors it expected a sale announcement in early 2022, but no such announcement came. By summer, Reeg shifted his tone when during its second-quarter earnings call he found investors and analysts’ focus on a deal “kind of amusing.”

“This is a change in you, not in us. This has been discretionary for us from day one, and it remains so,” he said, at the time. “If we have a trade that makes sense for us, we’ll do it. If we don’t, we’re fine waiting.”

In November, Reeg announced the company decided against a sale because the market wasn’t favorable and the cash flow of the asset considered for sale had continued to increase.

“Despite us talking about how this was a discretionary process for us, it created an unnecessary overhang in the stock,” Reeg said during the company’s third-quarter earnings call, while apologizing to shareholders.

The Review-Journal is owned by the Adelson family, including Dr. Miriam Adelson, majority shareholder of Las Vegas Sands Corp., and Las Vegas Sands President and COO Patrick Dumont.

McKenna Ross is a corps member with Report for America, a national service program that places journalists into local newsrooms. Contact her at mross@reviewjournal.com. Follow @mckenna_ross_ on Twitter.