Appraisals pre-empt some sales of houses

Is that gleam in your eye for a brand-new dream home?

There's a chance you might not get it.

The high number of foreclosures and short sales in Las Vegas have driven down appraised values to the point they're choking financing for new-home sales, sources in home building said.

Steep discounts are offered on "distressed" homes that are almost new, some of them having never been occupied, in the same subdivision where appraisers pull their data on comparable sales.

StoryBook Homes priced a two-story, 1,600-square-foot home in northeast Las Vegas at $115,000, but the appraisal came in at $102,000, principal and founder Wayne Laska said. The same appraiser had valued a similar home at $120,000 three months earlier, but it was single-story.

Everyone is disgruntled about property values in Las Vegas, especially homebuilders who have had sales canceled because a home didn't appraise at a certain value, said Amelia Hyden, president and chief executive officer of AMC of Southern Nevada, an appraisal management company.

Not every loan package is meant to be approved, nor is every home going to appraise at its asking price, she said. But when home appraisals come in below a sale price, the lender is unable to finance the deal. That leaves the homebuilder without a sale, and the buyer is unable to complete the transaction.

Appraising a home is not an exact science; it's an opinion, Laska said. One appraiser gives more value for a deeper backyard or driveway, and another gives them no value at all.

"I think the biggest problem with appraisers is they're not open to looking at their work and admitting they made a mistake or they need more information," the homebuilder said. "They're just not open to the seller or broker questioning how they arrived at the number."

FORECLOSURES AFFECT NEW HOME PRICES

Hanley Wood housing analyst Jonathan Smoke estimated that foreclosures and short sales affect net pricing of new homes in a submarket by as much as $90,000.

"In 2010, these properties sold at $49-per-square-foot less on average than typical resales or new homes, translating to a massive discount of nearly $90,000 on an average-sized home," he said.

"There are so many foreclosures available at lower prices, so it's hurting homebuilders and prices," Hyden said. "Just because you have a contract sales price, that does not mean that's the value of the property. Buying and selling a home is such an emotional experience. You have sellers who are emotionally attached to their home, and they'll put a value on it that's not market value."

Appraisers gather as much data as possible on sales in new-home subdivisions, and often builders don't provide data to support their values, she said.

Ryan Smith, sales manager for Shea Homes at Ardiente, said he sits down with each appraiser and educates them on energy-efficient features and "green" building techniques that might otherwise be overlooked in the appraisal process.

"It's been tough. We had one appraisal come in low, and the buyer agreed to bring in cash to close on the home," Smith said. "The underwriter for the lender has to challenge the appraisal and open it up to a board of appraisers, have them examine the appraisal and look at the properties used as comps."

Low appraisals have been an issue at Ardiente, an age-restricted community in North Las Vegas with 250 homes built by previous developer Centex Homes, Smith said. Shea had the good fortune of coming into the project without the legacy of a high cost structure, he said.

Homebuilder Laska said he gives as much information as possible to the appraiser.

"We're not trying to sway the appraiser, just make sure the appraiser is familiar with our product and the neighborhood," he said.

Real estate appraiser Ronald James of James & Associates said the market dictates new home values, not appraisals. He was assessing a foreclosure in northwest Las Vegas that looked like it had been lived in less than a year, and he could hear construction of a new home just down the street.

"If I can buy a house for $100,000 and you've got a house for sale next door for $50,000, and it's basically the same property, guess which one I'm going to take?" James said. "Until we get the economy stabilized, it's going to be up and down."

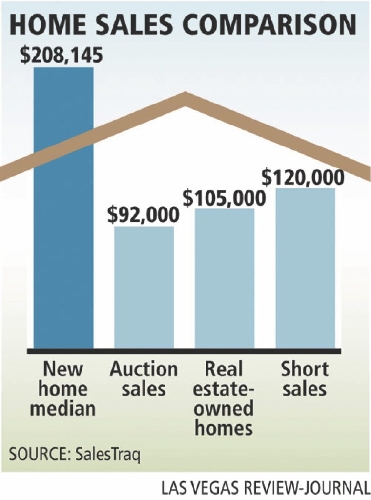

DISPARITY IN PRICES WIDEST EVER

The gap between new and existing median home prices in Las Vegas has widened to nearly $100,000, the largest it has ever been. The new home median for January was $208,145, compared with $92,000 for auction sales, $105,000 for real estate-owned homes and $120,000 for short sales, Las Vegas-based Sales- Traq reported.

New home sales have tanked since 2006 and are expected to remain depressed for years to come. Building permits plummeted to 3,776 in 2010 and got off to a slow start this year with 233 in January, according to SalesTraq.

Nationwide, builders started construction in February on the fewest homes in nearly two years and cut requests for permits to start new projects to a five-decade low.

That means supply will tighten. Already, scarcity in a few submarkets has hit a tipping point that has sparked demand. More broadly, the next several months will see waves of other markets flirt with insufficient supply and then flip, Hanley Wood reported.

Bob Denk, economist for the National Association of Home Builders, said new homes tend to be more expensive than existing homes, but it's not an apples-to-apples comparison.

You wouldn't compare a 15-year-old car to a new car, he said. Also, new homes are often built in the suburbs where a city is expanding. Denk said his condo in the center of Washington, D.C., is going to hold its value better than the last home built in a subdivision with a 90-minute commute into the city.

FORECLOSURE LOSSES EXPECTED BY BANKS

Foreclosures everywhere are having an impact on appraisals and making it hard for homebuilders to get funding for perfectly viable projects, the NAHB economist said.

"We've got one-third of our builders reporting they lost a job because the appraisal came in too low thanks to foreclosures," Denk said. "They've had a hard time getting financing related to the downward pressure on prices because of foreclosures."

Banks expect to lose about 40 percent on foreclosed properties, but in these horrible times, they're "taking it on the chin" to the tune of 60 percent discounts, Denk said.

"I'm sorry to say Las Vegas is the leader in this statistic," he said.

It's understandable that financing is hard to come by in high foreclosure markets such as Las Vegas and Phoenix, Denk said. But it's tough nationwide, even in states that produce energy and agricultural commodities, he said.

Appraisal manager Hyden said the market is correcting itself.

"We saw the boom in 2007, all the new homes popping up," she said. "The only way to correct that is getting this shadow inventory of REOs off the market. Eventually we will see an increase in new home sales."

Laska of StoryBook Homes said the home building industry will survive in Las Vegas, but business is a fraction of what it used to be.

"It's going to be competitive. We're competing with other builders, but more importantly, we're competing against the banks," he said. "They're the wild card, and what they do could influence the industry more than anything else."

Contact reporter Hubble Smith at hsmith@review journal.com or 702-383-0491.