Home prices hit new lows in valley, nation

WASHINGTON -- Home prices are hitting new depths in Las Vegas and most major U.S. cities and are expected to fall further over the next six months.

In a majority of metro areas tracked by Standard & Poor's/Case-Shiller, prices have fallen to their lowest points since the housing bubble burst.

High unemployment, stricter lending rules and fears that prices will continue to fall are among the reasons why few people are buying homes. A rising number of foreclosures are also weighing down prices. And as more people get stuck in depreciating homes, housing could slow the economy.

Across the country, the housing industry is recovering unevenly. Many of the cities now setting new lows have been struggling with high unemployment, more foreclosures and, in some cases, a delayed response to the housing bust in 2006 and 2007.

Homes in more established areas -- those that had little room to build during the housing boom -- are doing a better job holding their value. Coastal cities in California and the Northeast are seeing much smaller price declines. In Washington and San Diego, home prices even rose over the past year.

The median price of a resale home in Las Vegas was $119,000 in December, a decrease of $1,000 from November, Home Builders Research reported. However, the new-home median price rose to $218,080, a startling increase from $200,850 in November.

Excluding high-rise condo sales, which are typically much higher than traditional new-home product, the median price was $216,225.

Resale prices very likely could dip during the first half of 2011, housing analyst Dennis Smith of Home Builders Research said.

"If we believe what Fannie (Mae), Freddie (Mac), FHA and the big banks are unofficially saying, the market will see more foreclosed homes hitting the market in 2011," Smith said. "This would be a thorn in any local price recovery. However, it could work to improve sales velocities. There are still a significant number of investor groups who would like to buy properties in Las Vegas, and getting them at discounted prices is a very tempting carrot to dangle."

Still, many people who want to buy can't. Nearly 25 percent of households cannot move because they owe more on their mortgage than their home is worth, according to Capital Economics. An additional 25 percent can't qualify for a new mortgage because selling their homes would leave them with too little money for a down payment.

"We're likely to see new lows hit across most major markets at some point in 2011," said Mark Vitner, a senior economist at Wells Fargo Securities. "We're afraid of all this turning into another vicious cycle."

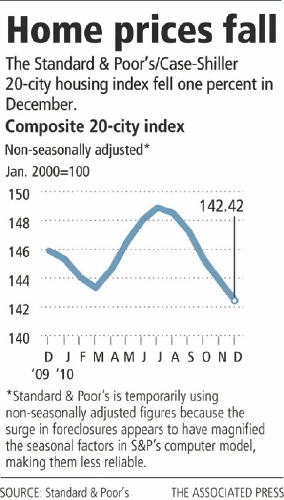

Housing prices in all but one of the 20 cities tracked by Standard & Poor's/Case Shiller fell in December from November. And the overall index declined for the sixth straight month. Washington was the only metro area where prices rose month to month.

Eleven markets hit their lowest point since the housing bubble burst in 2006 and 2007: Las Vegas; Atlanta; Charlotte, N.C.; Chicago; Detroit; Miami; New York; Phoenix; Seattle; Tampa, Fla., and Portland, Ore.

The housing sector is struggling even while much of the economy is recovering slowly but steadily. The latest evidence of the divide came Tuesday when the Conference Board said its Consumer Confidence Index rose in February to its highest point in three years. The report suggested that many people are more hopeful about hiring and income gains over the next six months.

By contrast, the outlook for housing this year is dim. Construction of new homes is on pace for little more than half the million units a year that economists consider to be healthy. And the number of vacant homes is near a record high.

Some of the worst declines in home prices are in cities hit hardest by high unemployment and foreclosures. A home that sold for $250,000 in Detroit in 2000, for example, now sells for roughly $163,150, according to the housing report. The unemployment rate there was 11.1 percent.

One in 24 Detroit-area homes with a mortgage was at risk of foreclosure last year, according to foreclosure tracker RealtyTrac Inc. -- the fifth highest rate among major cities.

Homes in Las Vegas, on average, have lost more than half their value since 2006. They now sell for less than they did in 2000. The city had a record-high 14.9 percent unemployment rate in December and led the nation in foreclosures last year.

Review-Journal writer Hubble Smith contributed to this report.