Housing slump will slog on, signs suggest

WASHINGTON -- Signs are emerging that the U.S. housing market's long slump is likely to fester through the summer, and the real estate market may not recover for at least another year.

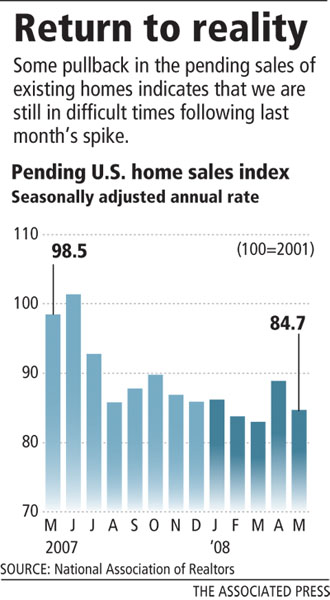

The latest report, the National Association of Realtors' pending home sales index, slipped by 4.7 percent in May to the third-lowest reading on record. The decline "suggests we are not out of the woods by any means," said Lawrence Yun, the trade group's chief economist.

The bad news came as the regulator for Fannie Mae and Freddie Mac tried to reassure investors that an accounting rule change wouldn't force the government-chartered mortgage finance companies to raise tens of billions in capital to offset losses.

With more negative data about the housing market continuing to emerge as the economy weakens and job losses accelerate, economists are reluctant to say the worst is over.

"Even if housing market activity does manage to bottom out later this year, it is likely that any recovery would be exceedingly slow," Jeffrey Lacker, president of the Federal Reserve Bank of Richmond said in a speech in Washington.

Although home sales are likely to fall to their lowest point late this year or early next year, any recovery is likely to be weak through at least 2010, said Mark Vitner, senior economist with Wachovia Corp.

Meanwhile, prices shouldn't hit bottom for another year at the earliest, Vitner said, since the housing market is glutted with unsold new homes and foreclosed properties.

Worsening matters, rates on 30-year mortgages have been above 6 percent since late May, leading to a steep decline in new applications.

The Realtors' seasonally adjusted index of pending sales for existing homes fell 4.7 percent to 84.7 from an upwardly revised April reading of 88.9. The index was 14 percent below year-ago levels. Sales are considered pending when the seller has accepted an offer, but the deal has not yet closed.

Wall Street economists surveyed by Thomson/IFR had predicted the index would come in at 87. The index, which sank to a record low of 83 in March, stood at 98.5 in May 2007. A reading of 100 is equal to the average level of sales activity in 2001, when the index started.

Pending sales fell around the U.S., sinking the most in the South, and the least in the West.

In Las Vegas, the number of units listed as "contingent" or "pending" declined slightly in the final week of June to 7,155, Las Vegas-based research firm Applied Analysis reported. That's more than double the number from the same period a year ago.

More than half of the 22,192 available units in Las Vegas' inventory were reported as vacant, while another 10 percent were occupied by tenants. Compared with a year ago, owner-occupied units represented the largest decrease from 12,226 to 8,429, down 31.1 percent, Applied Analysis reported.

Despite the negative numbers, "the worst of the hemorrhaging is behind us" and a modest recovery is likely to take shape next year, said Bernard Baumohl, managing director of the Economic Outlook Group.

Homeowners shouldn't get too excited, though, as Baumohl predicts median prices will show year-over-year gains of no more than 6 percent by next year.

By the Realtors' measurement, prices nationwide were down 6.3 percent in May, but are falling faster in big cities. The Standard & Poor's/Case-Shiller home price index of 20 cities fell by 15.3 percent in April compared with a year ago, dropping prices to their lowest levels since August 2004.

As the housing market and broader economy continue to sag, Senate lawmakers appeared on track to approve -- possibly by week's end -- a rescue plan designed to save hundreds of thousands of homeowners from foreclosure.

But it was still uncertain whether lawmakers would reach a deal with the White House, which is balking at key portions of the bill, particularly $3.9 billion included for buying and fixing up foreclosed properties. Democrats argue the money is key to preventing neighborhood blight, but most Republicans call it a bailout for lenders who helped cause the mortgage mess.

Review-Journal writer Hubble Smith contributed to this report.