Las Vegas area home prices edge up

The median price for both new and existing homes rose a fraction of a percent in July from the previous month, a hint that the housing market has flattened out in Las Vegas, a local analyst said.

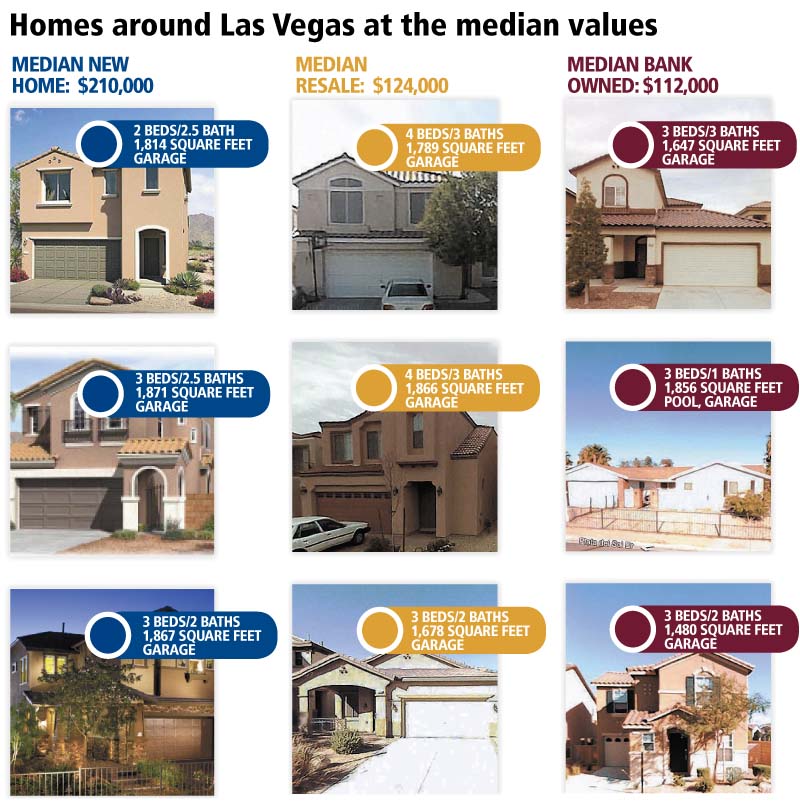

New home prices inched up to $210,000, from $209,000 in June, while resales went to $124,900 from 124,000, Las Vegas-based SalesTraq reported Wednesday. That is the first time existing home prices have gone up since February 2007, when they climbed to $288,000 from $$278,700.

The 0.7 percent month-over-month increase in resale price is "statistically insignificant" and could change with monthly revisions to the data, SalesTraq President Larry Murphy said. More importantly, it shows that prices have stopped falling, he said.

Steve Bottfeld of Marketing Solutions said the statistic might not seem like much, but to a market that has seen nothing but falling prices for the past 30 months, it's something to celebrate.

Prices have been traveling in a narrow $1,000 range for the past three months, suggesting they might be in the process of stabilizing, he said.

California and some pockets of the country have reported a slight rise in home prices also.

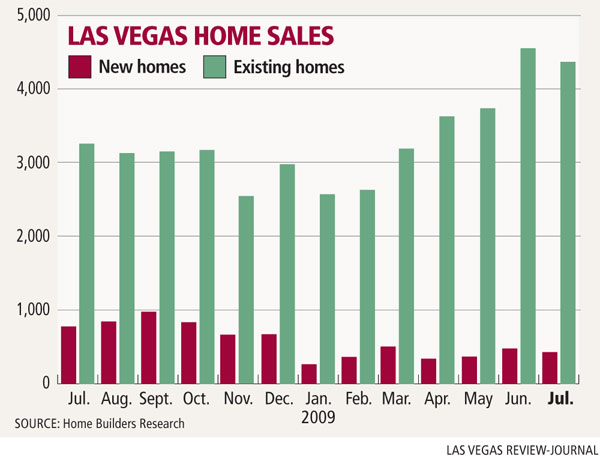

Sales of existing homes stayed strong in July with 4,675 recorded closings, the fourth consecutive month they have topped 4,000, SalesTraq reported. They are up 42.6 percent from the same month a year ago.

Nearly 60 percent of resales were bank-owned homes with a median price of $112,000. The remainder had a median of $140,000.

Home Builders Research counted 4,371 recorded resales in July, bringing the year-to-date total to 24,635, a 57 percent increase from a year ago. New homes sales are still lagging with 407 in July, leaving them down 58 percent for the year at 2,741.

One, two, even three months of data do not constitute a trend, Bottfeld said.

"Still, July appears to give some credence to the idea that residential real estate is beginning to recover in Las Vegas," he said.

California-based real estate consultant John Burns said any housing recovery will be W-shaped with the first leg up driven by the $8,000 first-time home buyer tax credit and improved affordability from lower home prices.

A "false peak" will form in November, he said. Sales and prices will fall again when the tax credit expires Dec. 1.

Burns estimates that sales will slow substantially in December and throughout the first quarter of next year because of the demand "pulled forward" by the tax credit. The market will stabilize when job growth turns positive, hopefully by next spring or summer, he said.

"While we believe there is another leg down, we don't believe that the decline will be that much further, so smart investments made with a long-term perspective should pay off handsomely," he said.

Murphy said he doesn't disagree with Burns' thinking.

"In my gut, I get the feeling there's another bobble or two after this stimulus of the tax credit wears down," he said.

Murphy said at least half of homes in Las Vegas are going to investors in cash deals for foreclosures.

It's tough for owner-occupants with limited financing to compete against guys such as Bob Schulman, chairman of Las Vegas-based Montecito Cos. He started a fund capitalized by institutional and high- net-worth investors to acquire 100 to 125 foreclosed homes in Las Vegas, targeting the Summerlin and Green Valley master-planned communities. Subsequent funds could acquire up to 500 homes.

Schulman said he looked at all potential real estate opportunities -- from new construction to value-added acquisitions of existing apartment, office and industrial properties -- and determined that the best value was to be found in single-family homes.

Not only had they overcorrected in price, they were substantially undervalued, he said.

"We looked at residential land here with homes on it, and they were 30 percent to 40 percent below the cost to build," Schulman said. "Why would I buy land? I can just buy the house with no risk."

Murphy said investors such as Schulman are really driving the entry-level market and taking those homes out of the inventory, which declined in July to 11,905 listings from 20,641 a year ago.

"Frankly, that's where the smart money is, and I can't fault them," Murphy said.

David Brownell of Keller Williams Realty in Las Vegas said the inventory of real estate-owned, or bank-owned, homes has been steadily shrinking in the past few months. The talk about the backlog of REO homes needs to become reality, he said.

"These properties need to begin working their way into the market," he said. "Until then, the options for today's buyer, especially the FHA loan buyer, are becoming significantly limited."

Nearly three-fourths of July home sales were bank-owned homes, and the current supply of those homes is about three weeks, he said.

"Hmmm. Calling it 'limited' may be an understatement. More like overly restricted," Brownell said. "Did I hear 'seller's market?' Some signs are starting to point us in that direction, even if only small ones."

Jeff Canarelli, vice president of sales for Las Vegas-based American West Homes, said he hopes the new home market has leveled off. American West is not building any homes on "speculation," or without a sales contract and deposit, he said.

The builder is selling new homes for $205,000, below the market median, with floor plans priced under $100 a square foot.

"Our attitude is people want a nice home with amenities," Canarelli said. "Still, (square) footage value is very important."

Contact reporter Hubble Smith at hsmith@reviewjournal.com or 702-383-0491.