New-home sales hold steady in LV

New-home sales in Las Vegas have been consistently low over the past six months and appear to have reached the bottom of the current down cycle, a local housing analyst said Wednesday.

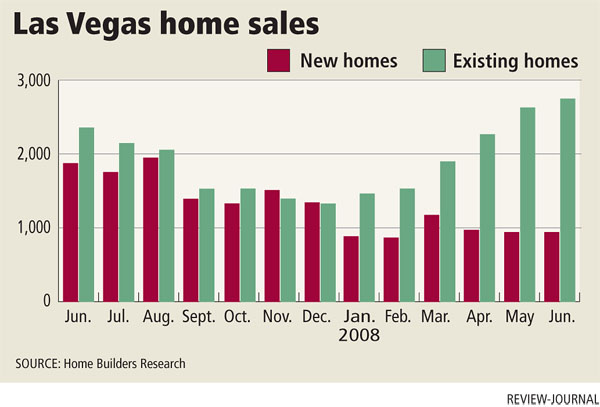

Dennis Smith of Home Builders Research counted 922 recorded escrow closings for new homes in June, bringing the total for the first half of the year to 5,747, a 45.1 percent decrease from a year ago.

Taking out 114 high-rise and mid-rise condos and 31 apartment conversions, sales of traditional single-family detached homes totaled 777, the sixth straight month under 1,000. The high mark of 3,233 came in June 2006.

This flat trend in new-home closing activity will be sustainable and will most likely continue through 2008 and well into 2009, Smith said.

"I've said before it's going to be a flat year. Before we see any recovery, it's got to stop going down, and it has," he said.

The median price of all new-home product sold in June was $269,900, a decline of $54,000, or 16.7 percent, from the same month a year ago. Smith said he doesn't see much of a drop in new-home prices.

"They can't build them for any less than they're selling for now or they just won't build them," he said.

New-home permits increased for the fourth straight month to 884 in June, but the year-to-date total is down 61 percent to 5,653.

Resale activity is picking up, topping 2,000 for the third consecutive month and increasing for the sixth straight month to 2,731 in June. The 12,500 existing-home sales through the first six months is down 15.9 percent from a year ago.

About 65 percent of resale closings in June were real estate-owned, or bank-owned homes, according to data from the Multiple Listing Service. The number of homes sold by the bank has increased 18 percent over the past three months, Smith noted.

As more real estate-owned properties hit the market, they will drive prices down and cut into existing-home sales, said Robert Lee, chief executive officer of Huntington Beach, Calif.-based Foreclosure Trackers.

"Say you've got two three-bedroom, two-bath model match homes," he said. "One's bank-owned for $300,000 and one's a resale for $400,000. Which one's going to sell?"

Lee, whose business is buying first mortgages from lenders when they go under, said a typical first mortgage might be $500,000 on a home that was appraised at $550,000, but an updated broker's price opinion puts the value at $320,000.

"You know what I'll pay for that loan? I'll pay $200,000," he said. "You're selling me a defaulted mortgage. How about document deficiency? Whatever the broker's price opinion comes in at, we'll pay 55 cents on that, max. That's the model."

The median resale price in June was $218,000, a decline of $62,000, or 22.2 percent, from a year ago, Home Builders Research reported.

Resale prices are still going to suffer, even as sales are going up, Smith said.

"The good news is an increase in sales, primarily because of lower prices, so the market's moving," he said. "We have to get rid of excess inventory. When demand equals supply, prices will start to go up."

As the inventory of real estate-owned and short sales increased, roughly tripling in both categories since the beginning of the year, lending institutions have become markedly aggressive in pricing homes to sell, said Frank Nason, president of Las Vegas-based Residential Resources.

In some cases, these properties are priced below comparable sales in the area, bringing in multiple offers. This has resulted in closings above list price, sometimes significantly more, Nason said.

Contact reporter Hubble Smith at hsmith@reviewjournal.com or 702-383-0491.